Chapter 2 : AI and Open Banking Working Together: When Theory Meets the Stack

The use cases are real. Here's what's actually working and what isn't.

If you missed Chapter 1, it’s worth reading first. We established a working definition:

AI, in this context, is a prediction engine operating at scale. Shared some AI terminologies in context of AI

We mapped it across the Open Banking stack (infrastructure, orchestration, experience)

We argued that the fintech executives building durable advantage are treating AI as infrastructure, not innovation theater.

Full chapter 1 is here :

This episode picks up where that left off. Because knowing what AI is in theory gets you about halfway there. The second half is knowing how it actually shows up in production.

Most popular terminology you hear that is either its “intelligent open finance,” or “AI-native banking,” or “agentic open banking” all collapse to the same practical loop:

Step 1 : Ingest consented data

Step 2: Apply the right form of AI

Step 3: Output a decision, insight, or action that a human or system can act on.

No magic. Just better signal extraction from data that was previously too voluminous or too fragmented for traditional rules engines to handle profitably.

From definition to deployment

Not all AI is created equal, and not every type belongs in every layer of the open banking architecture. Executives who treat AI as a single “technology” waste cycles and budgets. When companies say they’re using AI in Open Banking, they might mean any of four things:

They’re enriching transaction data using machine learning.

They’re making credit or fraud decisions using trained models.

They’re generating language based outputs ( summaries, insights, recommendations using large language models).

They’re beginning to orchestrate multi-step workflows using agents.

These are meaningfully different capabilities. Combining them without knowing well leads to bad procurement decisions, worse architecture choices, and unrealistic roadmaps. Separating them is the first job of any executive trying to navigate this space clearly.

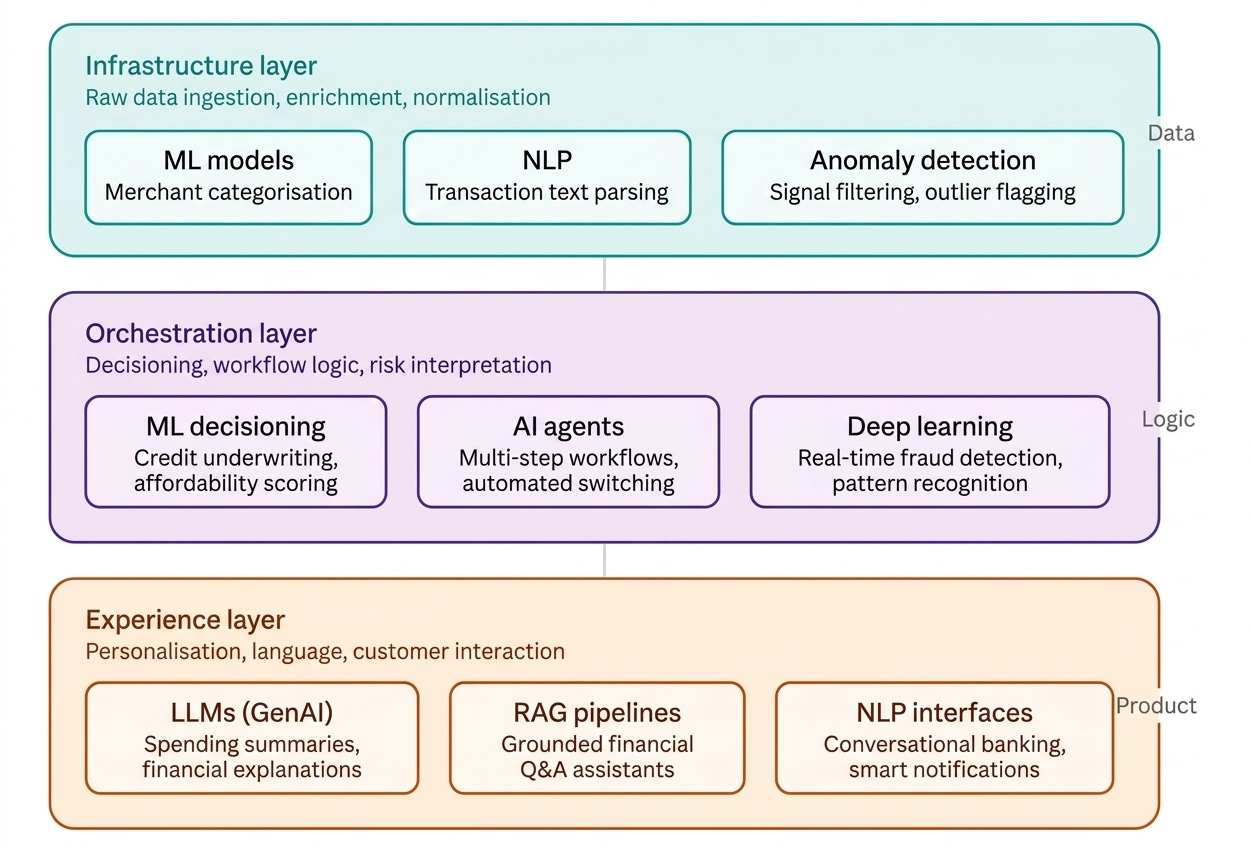

Where each AI type lives in the OB stack in details?

The diagram above maps this directly. The key insight is that not all AI belongs to all layers, and the failure to match AI type to layer is one of the most common strategic errors in this space.

At the Infrastructure/Data layer : The work is unglamorous but foundational.

Raw transaction data coming through Open Banking APIs is messy where merchant names are inconsistent, descriptions are cryptic, amounts are ambiguous without context.

ML models and NLP do the quiet work of normalising this signal: categorising merchants, identifying income streams, stripping noise.

Example : Plaid’s transaction enrichment engine. It processes billions of transactions and maps them into a clean, structured layer that becomes the foundation for every downstream product built on top.

At the Orchestration layer : AI becomes the decision engine.

This is where ML and deep learning replace static rules in credit scoring, fraud detection, and affordability assessment.

The decision is faster, more contextual, and improves as more data flows through.

AI agents are emerging here to handle multi-step workflows like automated account switching or recurring payment reconciliation that previously required human intervention or brittle rule chains.

Example : TrueLayer’s fraud scoring on payment initiation. Rather than applying generic fraud rules at the bank level, ML models trained on Open Banking signals assess each payment in real time before it reaches the PSP.

At the experience layer : The work becomes visible to the end customer.

This is where GenAI and NLP change the product surface.

It creates the personalization and interaction highly understandable to user: tailored insights, conversational interfaces, autonomous actions within consent.

Example : Monzo’s Trends feature uses GenAI to convert raw spending data into natural language summaries (not templated strings, but contextually generated sentences that reflect each customer’s actual behaviour.)

The mechanism underneath is RAG: a language model grounded in the user’s own transaction history so that the output is accurate and specific, not hallucinated.

ML remains the main engine for prediction at volume. DL powers the most complex pattern recognition in noisy transaction streams. NLP turns those signals into human readable explanations or chat interfaces. Gen AI creates tailored content or summaries on top of the enriched data. Agents represent autonomous systems that can plan and execute multi-step tasks while staying inside regulatory consent rails.

The architecture insight is simple:

The open banking API provides the raw material

The right AI primitive provides the interpretation and action layer.

Neither works at scale without the other.

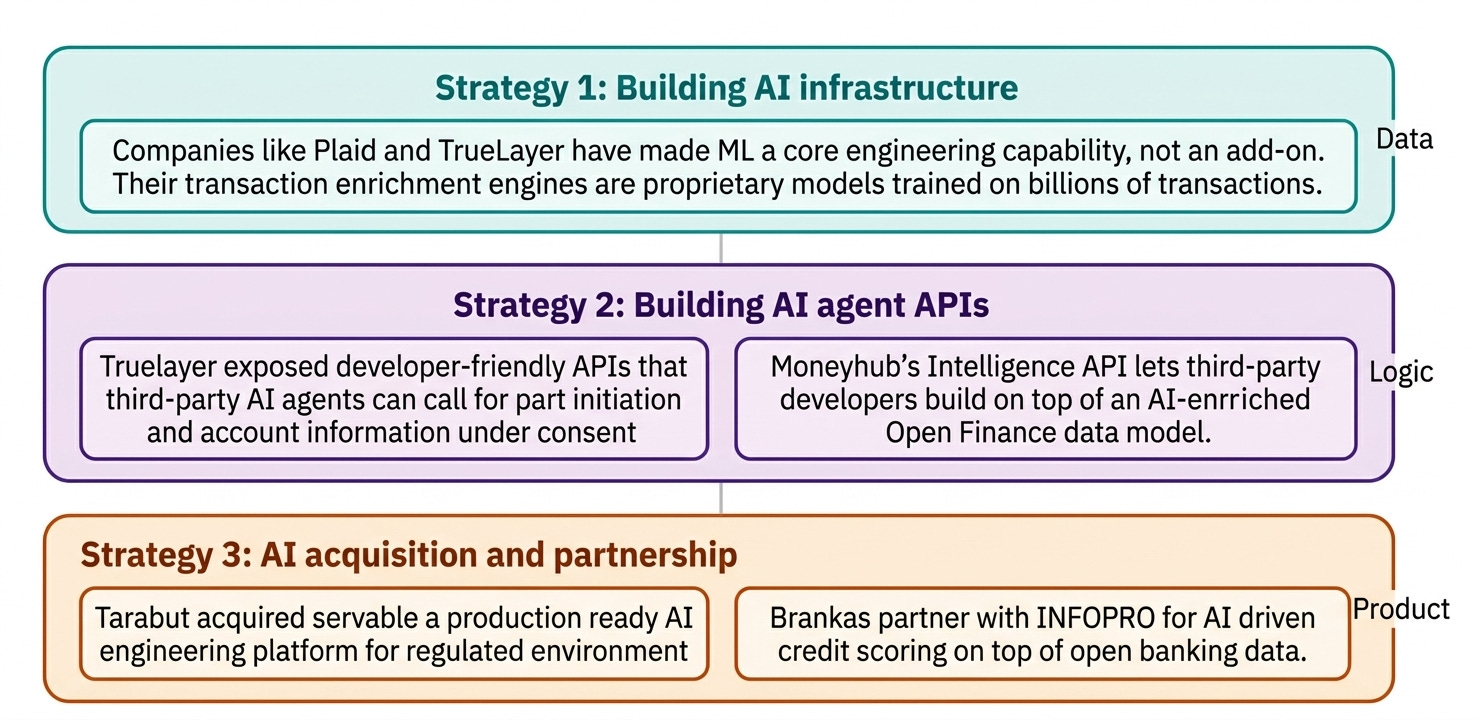

What Open Banking companies are doing right now?

Leading Open Banking platforms don’t have the same strategies. They are choosing focused strategies that match their strengths: API infrastructure, data scale, or customer relationships. One thing is sure, AI is not just the feature, but as a structural bet. The patterns cluster into three distinct moves :

The strategy image above shows concrete examples of how companies are combining AI with Open Banking right now.

The most durable investments are at the infrastructure layer. It improves the raw material that every downstream product depends on. This is high leverage because improvements compound across every partner using the layer.

The highest-profile moves are at the experience layer. AI handling the workload that previously required hundreds of agents. This is real, measurable, and strategically significant. But it only works if only clean, structured data underneath it.

The most interesting emerging plays are at the orchestration layer using agents. The concept of an AI agent that can take a goal and execute it autonomously across multiple API calls is still early. But the direction is clear.

These moves share a pattern:

Open banking specialist supplies the consented data rails

AI partner or internal team supplies the intelligence layer.

The economics shift from one off API calls to continuous, high-margin insight and automation services.

if you want to learn more about what happened in 2025 to early 2026, here you can read:

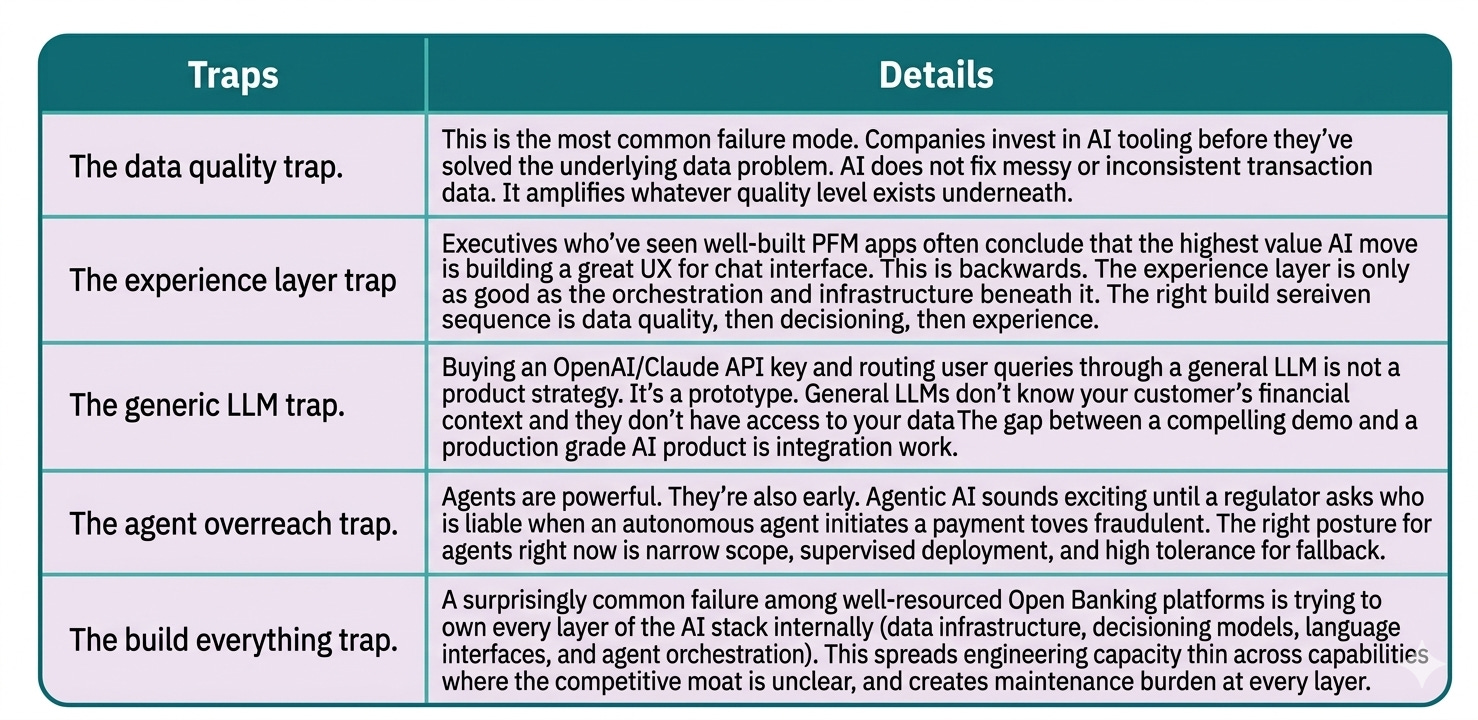

Where Open Banking companies fail with AI

Success stories make the headlines. The quieter reality is that most AI initiatives in open banking still stall. The traps are consistent and avoidable.The traps are specific, and they recur with striking regularity.

Studies in 2025 showed that as many as 95% of AI pilots in financial services never reach production. Banks often prefer to build rather than partner, believing internal control justifies the delay only to discover that model governance, continuous retraining, and regulatory attestations take far longer than anticipated.

The question is: which layer, if owned, creates the most defensible and compounding advantage? For most Open Banking companies, that answer is the data and orchestration layers. The experience layer can be assembled from best in class external components.

The use cases are not the strategy. They’re evidence for the strategy.

Infrastructure companies with the focus on API connectivity and data enrichment players build advantage through data volume and model iteration cycles.

Orchestration companies with decisioning, risk, compliance focus must build advantage through proprietary signals and model accuracy on high-stakes decisions.

Experience companies build advantage through user engagement, behavioural data, and the quality of the feedback loop between customer interaction and model improvement.

This series will continue to talk about AI across Open Banking use cases. The next we will try to understand Who Owns What?